Every corporate entity, in this period, is standing at the crossroads. They can keep following conventional work models. Or they can jump onto the tech bandwagon and breathe a new life to their enterprise.

To stay on the competitive edge, you have to opt for the latter. It is absolutely vital to redefine the business models and archetypes as a whole.

Traditional financial companies, and banks, in particular, are trailing behind the tech curve. As per an Accenture report, most big banks have systems as old as the 1970s and the 1960s. The new IT systems are patched on top of the core to deliver mobile banking capabilities.

Following the same suit, many companies in the corporate sector wait until technology matures. This causes them to lose out.

However, in the case of Blockchain, things weren’t as outdated. Traditional incumbents, along with tech propellants, knew this was going to be a big hit.

So, what is Blockchain technology?

Blockchain is a distributed, decentralized ledger that records the provenance of a digital asset. It is a system of reading information using a method that makes it challenging or impossible to modify.

It is a revolutionary technology because it reduces the risk, eliminates the risk of fraud, and brings transparency in a scaleable way. The transaction costs using Blockchain are a million times cheaper than transaction costs in the traditional economy.

Each block in the chain contains various transactions. Every time a new transaction occurs, a record goes into every participant’s ledger. This decentralized database managed by multiple participants is called Distributed Ledger Technology (DLT).

White and Case reports, Blockchain can enhance currency exchange, trade execution and settlement, supply chain management, micropayments, peer-to-peer transfers, regulatory reporting, and correspondent banking.

How is Blockchain transforming traditional business functions?

Industry leaders have recognized the ludicrous benefits Blockchain could bring to their ventures. The question is, what the potential of Blockchain is? How can we apply it across various verticals and transform the traditional business?

In this article, we will explore some radical changes brought by Blockchain for the businesses:

Redefining Financial Handling with Smart Contracts

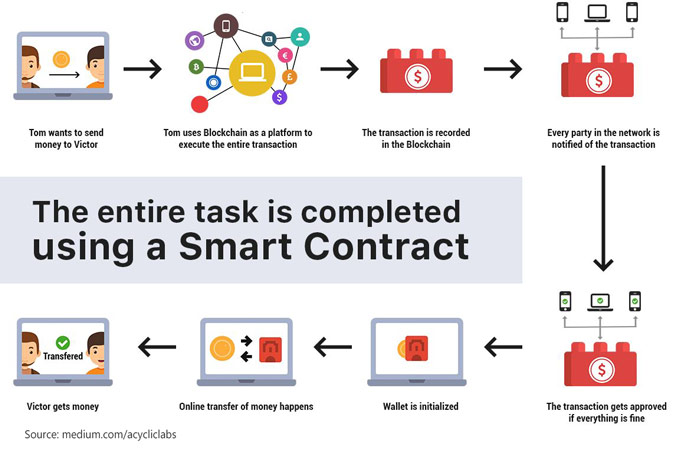

A contract, essentially, is a simple organism. When an offer is made to supply a product, the two parties accept the price and other associated terms.

However, executing these contracts can swiftly morph into complicated creations with several layers of dependency and several links connecting the parties.

For instance, when you are trying to purchase a property, think about all the hassle involved. It asks for verification of identities, transfer of money, etc. A smart contract will significantly change the way parties interact with each other.

Currently, smart contracts control transactions of digital currency. When translated into business, they can form an agreement between two parties. They can finalize pre-determined conditions before issuing payment to complete the transaction.

Let’s take the example of the relationship between a supplier and a service provider of a project. They can set conditions regarding material, quality, deadlines, and other commitments via Blockchain.

Upon delivery, the receiving party could check the purchase and transfer payment to the contractor. Smart contracts protect the two parties in this situation from forcibly transferring funds to the wronged side.

According to Market Research Future, Smart Contracts Market will probably hit 300 USD Million by 2023 with a 32% CAGR.

Smart Contracts, powered by Blockchain, are not an ordinary escrow service. It eliminates the need for manual input and updates legal ownership records automatically.

Increased Security Enhances Market Operations

Blockchain is the hottest thing in the corporate world—one of the significant reasons for beings its stellar secure framework. Cryptography is the basis of this technology. It can improve data protection and security to the highest degree.

Its distributed nature allows checking signatures on the entire network nodes' ledgers and verifies they haven’t been changed. If someone tries to change the record, it renders their signature invalid.

Not only this, but data on Blockchain is virtually impossible to hack. Every legitimate transaction received confirmation from multiple nodes on the network. A hacker needs to infiltrate via all nodes, which is technically impossible.

This feature of Blockchain technology has compelled many entities to accept its adoption across their entire model. Many storage service companies are assessing ways Blockchain can protect data from hackers. Apollo Currency Team is an excellent example of an organization that has embraced Blockchain technology in its system (The Apollo Data Cloud).

Its enormous security potential is perhaps one reason why Gartner suggests that Blockchain’s business value-addition will reach $176 billion by 2025.

Helps to Manage Human Resources

As Blockchain technology becomes more mainstream, HR professionals will soon find it disrupting their daily workflows. Human Resource professionals, in general, are dealing with planning, recruitment, interviewing, and training. They work along with executives on strategic planning, training, and compensation.

The Society for Human Resource Management shared insight regarding the application of Blockchain to HR. It stated that Blockchain could help HR professionals to verify the credentials provided by the job candidates and existing employees.

The association also anticipates Blockchain can prevent third-party companies from providing inaccurate data about the candidates.

Following are some of the ways that Blockchain will impact HR in beneficial ways:

- It Protects HR from Cyber Criminals – The ability of criminals to gain access to employees’ data is reduced. Hackers cannot access or corrupt the data.

- It Transforms the Recruiting and Hiring Process – Applicants can provide employers with permission to access their Blockchain-based employment data. This may include letters of recommendation, employment history, educational background, and much more.

- It Can Improve the Accuracy of Time and Attendance Data – It ensures that records are accurate and impervious to malicious entities. The information saved in the system through attendance and data is accurate and cannot be tampered with.

An example of a Blockchain-based payroll system presented by Workchain gives us a lot to learn from. It enables the workers to receive their paycheck as soon as they complete their work. It provides employees with an automated payroll solution that reduces costs and improves efficiency.

Improves Digital Marketing and Advertising

One of the most intriguing aspects of Blockchain is that it gives the value of data back to the consumers. So far, many companies have benefited from being able to pull the data from their customers.

From the local café down the street to larger companies like Walmart – everyone wants our phone numbers, postal address, and email address. It helps the companies know more about their consumers and market them personally.

Another aspect of Blockchain helping with marketing is its role played in reducing security risks. According to Juniper Research, advertisers expect to lose 44 billion USD by 2022 due to frauds. The Blockchain-powered systems can reduce “click-frauds,” gradually enabling the marketing executives to hit their targets.

Moreover, Blockchain also allows consumers to probe into the backgrounds of a product or service. They can find where an item was manufactured or grown. They can also determine what kind of soil it grows on and how much the workers get paid. This is a massive development in the present age as consumers care about manufacturing integrity before purchasing.

We have a fantastic example of Blockchain usage in the case of IndaHash. It is an online platform that enables brands to reach digital influencers. By connecting influencers and brands, it helps the deployment of authentically branded campaigns in a scalable manner.

To sum it up, the real impact of Blockchain in digital marketing is not in the development of new cases. It is how these cases will impact entire systems that have popped to manage the digital marketplace. When digital marketing is growing by the moment, the Blockchain changes this scenario in a disruptive manner, perhaps even in irreversible ways.

Easier for Small Companies to Build Trust

It can be challenging for small companies to stand out, especially when market sharks are swimming around you. Many consumers are wary of businesses they haven’t heard of before.

Nonetheless, Blockchain will flip the scenario. Reputable businesses can use it to establish trust, no matter how small they are. They can prove where their products are coming from and display every step of the supply chain. This enables consumers to know what these companies are providing. And they may be more willing to buy from them instead of their competitors.

It also helps to establish a positive reputation in the industry by resolving disputes with efficiency. This saves judges, lawyers, and clients a lot of time. Blockchain could be the gateway to generous amounts of data that could enhance a firm’s ability to find evidence or disparities in their legal cases.

An incredible example of legal use case is Legaler. It is a platform that offers encrypted communication between clients and legal advisors and highly secure storage for the documents. It allows direct collaboration on the papers.

Hence, small business owners can adopt Blockchain to beat the market sharks and establish their credibility in the industry through inventive methods.

Parting Thoughts

The Blockchain hype is higher than ever. Many players are looking forward to its adoption. When more companies try to leverage this technology, we will indeed find some spectacular developments in the future. There is an industry-wide excitement to push Blockchain forward. We shall witness extraordinary economic growth if the companies learn how to get around and use it to their avail.